What does the New Tax Year mean for me?

April is turning out to be the best month ever! The weather is warming up; lockdown restrictions have been lifted, and it's the start of the new financial year.

For most people, the new financial year doesn't mean much, but it should. With each new tax year, your tax allowances and tax relief schemes reset, meaning it's the perfect time to get ahead and plan your financial goals for the year. However, we understand that many of us aren't that clued up when it comes to money management, and that's ok. No one teaches you this stuff at school, and that's why StepLadder is here to help.

Stick with us and we’ll break down the different kinds of income as well as some of the Government schemes you can leverage which are tax free. That’s right, tax free! So pop the kettle, sit back and take some time out for yourself.

Understanding income

To start, did you know there are 3 types of income? Earned, Portfolio and Passive income. It's important to understand the different kinds; doing so gives you the knowledge to edge one step closer to financial freedom. Here's a breakdown of what each type of income means:

Earned income

This is income that you receive in exchange for your skills and time, such as salary/wages, commission, bonus or consultation services. Don't forget you could also be entitled to tax relief, so visit .Gov to find out what you're entitled to.

Portfolio income

This is income that's generated through investments. Examples include ISA's/LISA's, stocks and shares, index funds, pensions and property.

If you want to generate income through investing, start by working out how much of your annual income you want to invest and get some advice from people in the know. But remember, investments can go down as well as up - so take it seriously.

Passive income

This income is generated in the background, simply by owning assets. Examples of this include rent (if you’re a landlord), side hustles, affiliate marketing, publishing a book or advertising on your website. These pots may not be much, but they all add up. Find ways to increase your streams of income to build up your passive income.

Important note: with different types of income comes certain tax requirements and declarations. If you intend to maximise your income and allowances spend the time familiarising yourself on the Tax and Benefits section of .Gov.

So now you know the different kinds of income, are you missing any tricks? Is there more you could be doing to maximise your financial future.

Now let's talk about tax. The dreaded word we all hear where the tax man or woman comes and takes your hard-earned cash. No one likes being taxed, but you can maximise your income streams if you know what to watch out for. For most people in the U.K, the standard personal allowance is £12,500, which is the amount of income you won't get taxed on. Your Personal Tax allowance may be bigger if you're entitled to:

Get up to £125 back if you're WFH

You don't get a payout, but if you're eligible, HMRC changes your tax code, meaning you pay less tax. Visit the Government's Money and Tax section for more info.

Challenge your Council Tax Band

Nearly half a million homes across the U.K could have the wrong tax band. Citizens Advice has all the details. Martin Lewis, the MoneySavingExpert, spoke to one viewer who received a £1,400 refund.

Stop paying interest on credit cards

Research Balance Transfer credit cards. These work by moving debt to a different credit card with a 0% interest in return for a small fee. Use the eligibility checkers first, so it doesn't impact your credit score.

Leverage the Marriage Tax scheme

Being married comes with perks. If your partner has taken a financial hit by the pandemic, you can transfer £1,250 of your Personal Allowance to a husband, partner or wife. T&C apply via .GOV

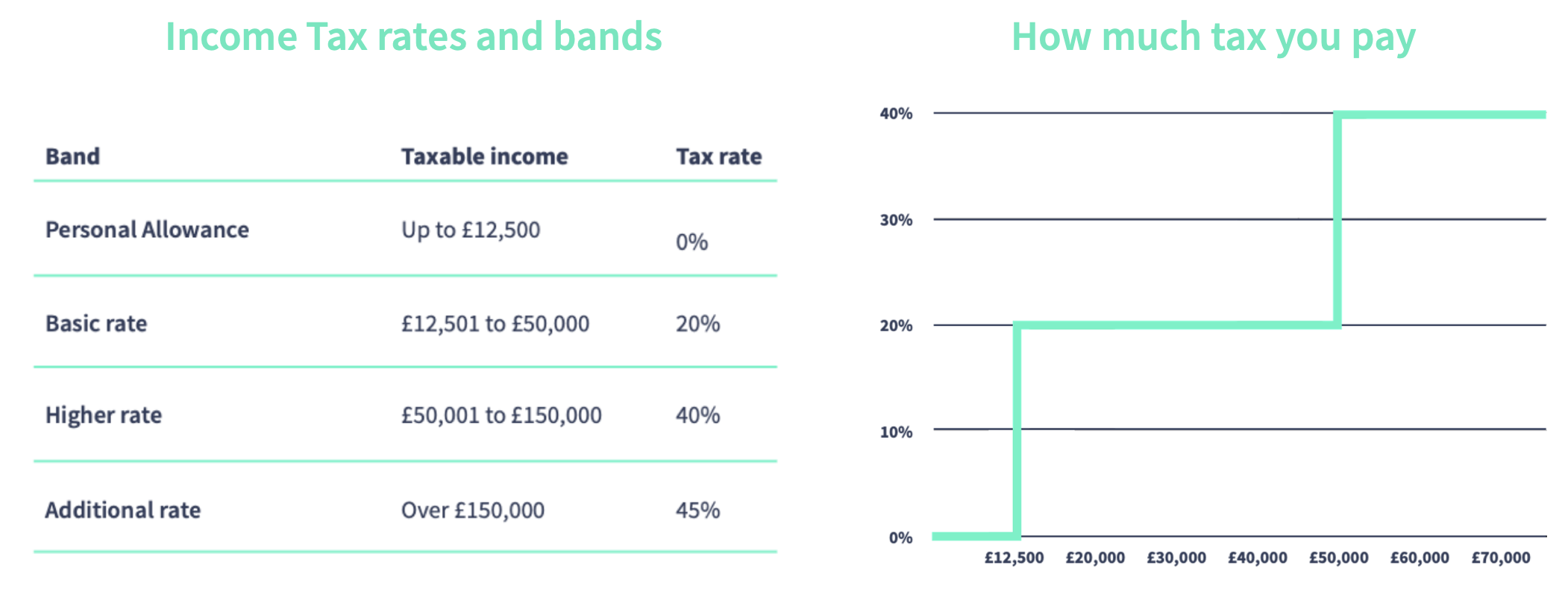

But how much tax will I pay each year? Well, that's where income tax rates and bands come in. The table below shows how much tax you pay in each band if you're eligible for a standard Personal Allowance of £12,500. For those living in Scotland, the income tax bands are different.

The majority of us get taxed either at the 20% or 40% tax band. For those who earn between £12,501 to £50,000, you'll be taxed 20% per pound. And for those who make between £50,001 to £150,000, you'll be taxed 40% per pound.

But wouldn't it be great if there was a way we didn't have to pay tax or certain things? This is where your tax-free allowances come in, starting with ISA's.

What is an ISA?

An ISA stands for Individual Savings Account, and there are 4 types of ISA; Cash, Stocks & Shares, Innovative Finance and Lifetime ISA's. Here's what each one does:

Cash ISA

This is a type of savings account that lets you earn interest on your savings without paying tax. You can invest up to £20K into an ISA throughout the tax year, and each year the allowance resets!

Stocks and Shares ISA

While many people prefer a cash ISA for security, you can also invest in shares, bonds from various companies pooled into one investment or shares in individual companies. Naturally, this investment is a little riskier, but that's the gamble you take for higher returns.

Innovative Finance ISA

Here, you lend your money to borrowers in return for a set amount of interest if you're prepared to not touch it for a while. This type of ISA is a form of peer-to-peer lending. If you commit to this option, your investments are matched up with borrowers such as businesses, individuals or property developers.

Lifetime ISA

You can use this type of ISA to help you buy your first home. You have less flexibility with this ISA where you can't easily access the money; however, if you commit to it, the Government will add a 25% bonus to your savings, up to a maximum of £1K per year.

Another way you can get a few pounds back is if you have a child. Not to be mistaken by Ib's, but if you're a parent or guardian, you can get up to £500 every 3 months (up to £2K a year) for each child to help with childcare costs. This goes up to £1K every 3 months if a child is disabled (up to £4K a year).

But what can I use Tax-Free Childcare for? You can use it to pay for approved childcare, for example:

- childminders, nurseries and nannies

- after school clubs and play schemes

Your childcare provider must be signed up to the scheme before you can pay them and benefit from Tax-Free Childcare. Check with your provider to see if they've signed up and visit. Gov for more info.

And our last piece of knowledge we want to share is for people who may have a business/side hustle or anyone who's considering starting one. Did you know you can get advice and financial help from government-backed schemes?

If you're self-employed, you can also get:

- help with tax

- regional help with exporting

- advice on writing a business plan

If you're unemployed or on benefits, you may be able to get extra help through your Jobcentre Plus work coach. Suppose you're thinking about starting a side hustle or your own business. Take the time to visit .Gov to see what support you're entitled to.

Our recommendation is to go and spend some time looking on the Government's website. It's a great resource to understand what schemes you can leverage for your finances.

And of course we think a great way of maximising your finances could be to join a StepLadder Circle. You can do this by putting as little as £25 per month away, which can help you achieve your financial goals.